Everyone is in for it and it seems no one wants to miss out. Recent popular activity on Wall Street has been raising the price target for Nvidia (Nasdaq: NVDA) Involved. After a hugely successful 2023 based on exceptional results, driven by its position as the undisputed leader in AI chip manufacturing, analysts have recently adjusted their models, raising targets based on the belief that the AI opportunity has not yet been fully realized.

However, without actually needing any adjustments, Ananda Baruah, a 5-star analyst at Loop Capital, decided to jump right in and cancel all other forecasts.

The senior analyst recently initiated coverage on NVDA stock with a Buy rating and a $1,200 price target, suggesting the stock has room for further growth at 65% from current levels. (To watch Baruah's track record, click here)

What is driving Baruah's bullish position? “Not only do we believe there will be a material uptick in Street estimates in FY2024/FY2025 and FY2025/FY2026, but we are on the front end of GPU compute and foundational build of AI generation across Hyperscale for 3 to 5 years,” the analyst explained. . “While we acknowledge that additional silicon providers (private as well as AMD and INTC) and Hyperscale's own in-house silicon solutions will come online over the next few years, our work indicates that NVDA's largest customers will take whatever NVDA can offer them in Years 2024 and 2025.”

With data center GPUs, Baruah expects FY2024/FY2025 revenue and EPS of $132.4B, $30.00, compared to the Street's $95.8B, $21.76. In FY2025/FY2026, Barroa expects these numbers to be $175.6 billion and $40.00, versus consensus of $110.0 billion and $24.84, respectively.

If that's not bullish enough, with revenue and GM expansion, Baruah also believes there is “legitimate upside potential even to our above estimates.”

While the immediate reaction is to think that Baruah may be exaggerating here, it's worth noting that since the generative AI opportunity took off a year ago, Nvidia's quarterly results show a “distinct pattern of clear rhythms.”

The reason Barua is more confident from the general Wall Street standpoint is fairly simple. Essentially, Baruah believes Nvidia is poised to sell far more high-end data center GPUs than other analysts currently expect. For FY2024/FY2025, Barua sees Nvidia tracking around 5.0 million (and 6.5 million+ for FY2025/FY2026). Based on investor conversations, Baruah believes the Street expects a total of 4.0-4.5 million enterprise and data center GPUs over the same period.

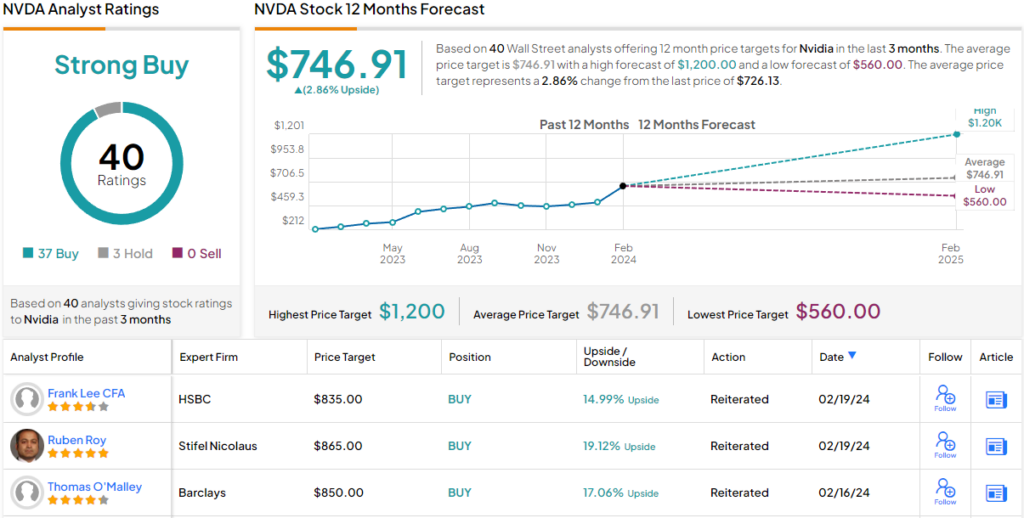

Given the collapse of consensus, most of Baruah's colleagues are leaning towards the upside as well. Based on 37 Buys against 3 Holds, the stock has a Strong Buy consensus rating. However, some seem to think a cooling-off period for the stock is appropriate; The average target of $746.91 suggests shares will remain range-bound for the time being. (be seen Nvidia stock forecast)

To find good stock trading ideas at attractive valuations, visit TipRanks' Best Stocks to Buy, a tool that unites all of TipRanks' equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

“Typical beer advocate. Future teen idol. Unapologetic tv practitioner. Music trailblazer.”

More Stories

JPMorgan expects the Fed to cut its benchmark interest rate by 100 basis points this year

NVDA Shares Drop After Earnings Beat Estimates

Shares of AI chip giant Nvidia fall despite record $30 billion in sales